Seen a collection account on your credit report?

A single line in the Collections section can drop your credit score dramatically.

And it happens even if you:

have never heard of the debt

believe it’s a mistake

see a company you don’t recognize

recently moved

never received any letters

This is a common situation.

The key is to start the protection process correctly.

You will need this information to fill out your letter.

official / federally authorized websiteт AnnualCreditReport.com and fill out the form

Find the collection entry (free)

You don’t need to download the file — opening the entry and taking a screenshot is enough.

Open your Experian, Equifax, or TransUnion report.

1

If it's not in one report — check the other two.

Each bureau keeps its own database.

Each bureau keeps its own database.

Look for these sections:

Collections

Negative Accounts

Derogatory Marks

Potentially Negative

Open the account details and write down the collector’s information.

In the account details, you’ll see:

the company name

address

Account Number

Balance

step 1

1

2

1

2

3

1

2

3

4

step 2

Stop. Do not call and do not pay.

A collector can promise anything —

but verbal promises cannot be proven later.

Why you should NOT pay

Even a small payment:

may be treated as confirming the debt

changes the status to “Paid Collection,” which is still negative

does NOT remove the entry

takes away your right to request documents

Why you should NOT call

Phone conversations:

create no evidence

have no legal weight

lead to “your word vs. their word”

are often used to pull you away from official procedure

The correct first step is a formal written request.

A Validation Letter is a legally protected procedure.

You formally demand an explanation of why this negative item exists.

step 3

Send an official request

You have the right to request from the collector:

Verification documents

Debt / account history

Proof they have the legal right to collect

How to send an official request

Why write to the collector at all?

typing

A collection entry can lower your credit score and stay on your report for 7 years

It will not disappear by itself.

Validation Letter

is the simplest and safest way to stop the collector and check whether they actually have the required documents.

In many cases, this step alone is enough:

if no proof exists, the entry may be reconsidered without further actions.

This is not a guarantee of outcome —

but it is the official legal mechanism for checking the accuracy of data.

In those situations:

An Important Industry Fact

Many collectors buy debts in bulk, often with limited documentation.

Sometimes, they do not have the full set of documents supporting the debt.

Sometimes, they do not have the full set of documents supporting the debt.

How it works:

If the debt is “fresh”:

— collection activity must temporarily pause until they respond.

If the debt is older:

— the Validation Letter becomes a formal request for information.

collection may be paused

the information can be disputed

credit bureaus may reconsider the entry if it is not verified

within 30 days after the first written contact

WHY IT COSTS $29

correctly

officially

without mistakes

without a lawyer

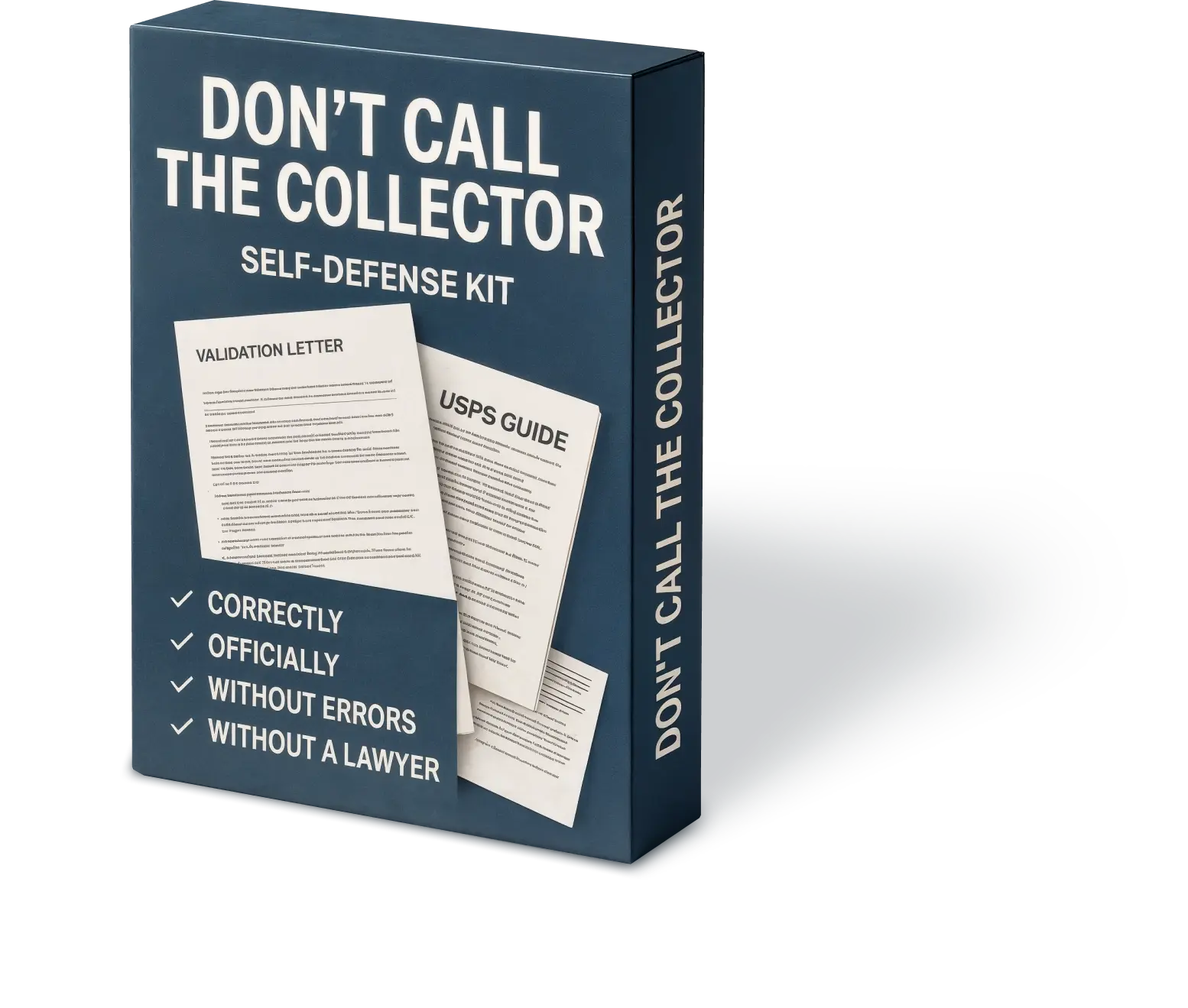

We created a complete kit that helps you go through the procedure:

About our product

The kit includes:

Validation Letter (ENG)

A legally compliant template written according to FDCPA requirements.

Intended for use in all U.S. states.

“Anti-Robot” handwritten method

Key fields are left blank.

You fill them out by hand in block letters so that:

• OCR scanners do NOT classify it as an internet template

• the request is guaranteed to reach a real employee

• your letter receives proper attention

• OCR scanners do NOT classify it as an internet template

• the request is guaranteed to reach a real employee

• your letter receives proper attention

Letter breakdown & filled-out example (ENG / RU / ES)

You understand every paragraph of the letter you send.

All explanations are available in three languages.

All explanations are available in three languages.

Step-by-step USPS guide

We explain:

• which forms you will receive (PS 3800, PS 3811)

• where to put the checkmarks

• what to say to the USPS clerk

• how to get tracking and proof of delivery Correct mailing is what makes your letter an official legal document.

• which forms you will receive (PS 3800, PS 3811)

• where to put the checkmarks

• what to say to the USPS clerk

• how to get tracking and proof of delivery Correct mailing is what makes your letter an official legal document.

Comparison:

Lawyer

$150–300

per letter

Credit Repair services

$100/mo

and often drag the process out

Don’t Call the Collector

$29

All-in-one solution

You get the tool for $29 — a one-time purchase.

This is the price of peace of mind, control, and a proper start.

Customer reviews

Aleksei

New York

USPS guide helped me understand the forms — I would’ve definitely made mistakes alone.

After the letter, the collector sent an official response, and the issue was resolved.

Carlos

California

I managed to complete the whole process myself.

The letter was clear and strong.

Feels like I’m in control for the first time.

Who this kit is for

if you’re not sure the debt is yours

if you want calls to stop

if English communication is difficult

if you want an official, risk-free solution

if the debt is old and hurting your score

if you do NOT want to pay without seeing real documents

You will receive your kit.

For convenience, we also send the same download links (files included) to your email, so you can save them to a folder of your choice.

Once the payment is completed, a download page will open (PDF file).

You’ll eventually need:

• Collector name

• Mailing address

• Account number

• Balance

• Collector name

• Mailing address

• Account number

• Balance

Step 1 above shows exactly where to find them.

If you don’t have these yet — that’s normal.

• check Spam

• Still nothing? Write to us with your order number — we’ll resend manually within 15–30 minutes.

• Still nothing? Write to us with your order number — we’ll resend manually within 15–30 minutes.

If you don’t see the email:

Delivery guarantee

What you’ll need later

Want to help improve the materials?

If you used the kit and want to share your experience — email us.

Do not send personal documents or your credit report — text only.

We wish you clarity and peace of mind throughout this process.

We wish you clarity and peace of mind throughout this process.

Don’t Call the Collector” is not a law firm and does not provide legal advice.

We offer self-help materials and educational information only.

Use these materials at your own discretion.

For legal advice, consult a licensed attorney.

digital goods are non-refundable once delivered.

Refund policy:

Email: